The factor-fee argument is the single most consistent piece of leverage carrier defense uses against funded contractor invoices in Florida. It does not appear on every file. It does not have to. It appears on enough files, and works often enough, to materially affect default rates and recovery percentages across funded portfolios. Most claim-funding companies have seen the pattern in their own data without necessarily naming it as a single phenomenon.

This is a technical piece about a financial-legal argument and what to do about it operationally. It is not a critique of factoring or funding economics. The math of advancing capital to restoration contractors and adjusters is what it is. The piece focuses narrowly on the documentation and estimating decisions upstream of the funded invoice — because that is where the factor-fee argument is won or lost.

What the factor-fee argument actually says (and what it doesn't)

The argument has two distinct forms, and they tend to be used in combination rather than separately.

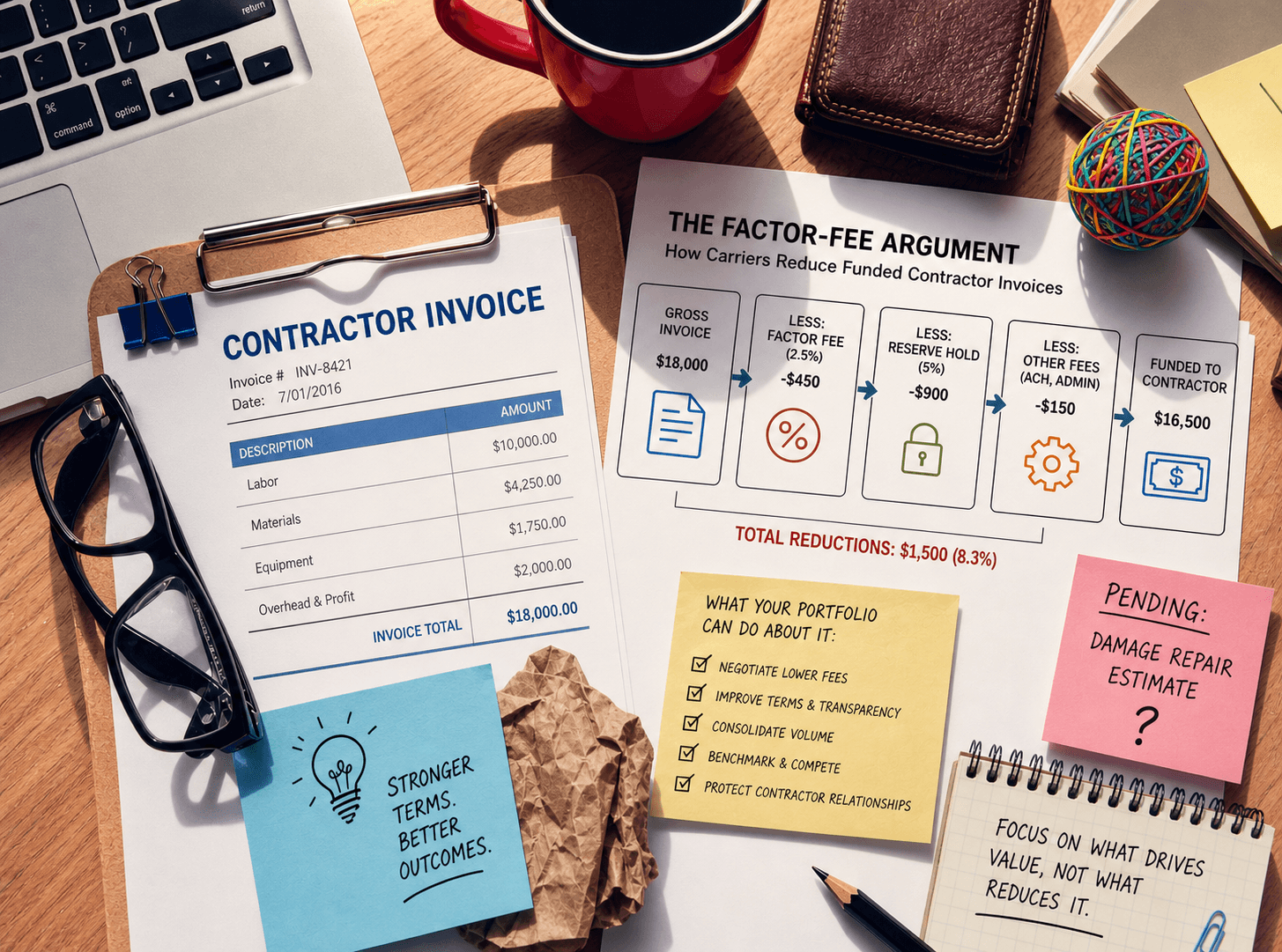

Form one — the inflation argument. When a contractor finances their receivables through a factor, the factor charges a fee, typically in the range of 18% to 25% of the receivable value. Carrier defense attorneys argue that this fee represents a financing cost the contractor has chosen to incur, and that the contractor is now passing this cost through to the carrier in the form of inflated invoice amounts. The argument's structure: "the contractor's invoice is X, but the contractor only needs Y to cover their costs and profit; the difference is the factor fee, which the carrier did not agree to finance."

Form two — the credibility argument. The same factor-fee relationship is presented as evidence of the contractor's financial fragility — a contractor who needs to factor their receivables is, by implication, a contractor whose business model is unsustainable, whose pricing is unreliable, or whose work product cannot be vouched for at face value. The argument's structure: "this contractor's choice to factor signals that the invoice is not a market-rate document but a survival document."

Neither argument is technically valid in most cases. Both arguments are sometimes effective in negotiations and in court. Both arguments are designed to create leverage, not to establish truth.

What the arguments do not say — and where they fall apart on substance — is that the work was unnecessary, that the documentation was wrong, or that the categorization was incorrect. The arguments target the financial structure around the invoice, not the technical content of it. This is the seam where the technical fix lives.

Why funded contractors face this argument and unfunded peers don't

The factor-fee argument requires the existence of a factor fee. An unfunded contractor doesn't expose this surface. A funded contractor does, the moment the carrier or carrier counsel becomes aware of the funding relationship.

This creates an asymmetric exposure pattern that funding companies rarely see in aggregate, because each individual contractor relationship presents the issue independently. The funder sees default rate. The funder sees recovery percentage. The funder may not see, in the data, that the contractors in the portfolio are facing a specific argument that their unfunded competitors are not facing.

The disclosure trigger varies. In some Florida files, the funding relationship becomes visible through assignment of benefits documentation. In others, it becomes visible through subpoenaed records during litigation. In still others, it becomes visible through Letter of Representation language or Direction to Pay structures that reference the factor.

Once the factor relationship is disclosed, the argument becomes available. The probability it gets used scales with the disputed value of the file and the carrier's defense posture on the case.

The two carrier playbooks

Carrier defense attorneys deploy the factor-fee argument through two operational playbooks, depending on the case posture.

Negotiation playbook. The argument shows up in pre-suit negotiation as a justification for a reduction offer. The carrier representative cites the factor fee as evidence that the invoice is inflated and proposes a settlement at a discount that approximately equals the factor percentage. The contractor — or the funded chain — accepts the reduction or escalates to litigation. In most cases, the reduction is accepted because the contractor or PA has cash flow pressure that the carrier knows about.

Litigation playbook. The argument appears at deposition of the contractor, the public adjuster, or the funded relationship principal. The questioning sequence establishes that funding exists, establishes the factor rate, and lays predicate for the inflation theory or the credibility theory at trial. The deposition transcript becomes negotiation leverage at mediation.

Both playbooks share an operational characteristic: they rely on the documentation around the invoice not establishing strong technical defensibility. When the underlying estimating documentation is weak, the factor-fee argument has room to do damage. When the underlying estimating documentation is technically defensible at every line item, the factor-fee argument loses traction because it does not engage with the substance the technical documentation establishes.

The technical fix: documentation that closes both arguments at intake

Both the inflation argument and the credibility argument rely on the absence of independent technical justification for the invoice. If the invoice can stand on its own technical merit — if every line item is correctly categorized in Xactimate, if every code reference is current and properly cited, if every mitigation step is documented under appropriate ANSI/IICRC framework — then the financial structure around the invoice becomes irrelevant to the merits.

The carrier's defense team can still bring up the factor fee. They cannot use it to reduce a line item that is independently defensible.

The fix in operational terms involves three layers:

Layer one — the underlying invoice. Written in Xactimate at correct sub-line specificity. Code citations current to the 8th Edition of the Florida Building Code (2023). Mitigation work documented with daily psychrometric logs (water), protocol citations (mold, fire), and itemized PPE/supplies/disposal. This is the technical floor.

Layer two — the methodology disclosure. A separate Audit Report and Variation Report consistent with Florida Rule 69BER24-4 that establishes how the estimate was constructed, what frameworks govern, and what evidence supports each line. This document exists outside the invoice and travels with it through review and litigation.

Layer three — the inspection evidence base. Photographs in a documented grid, dimensional records, and on-site inspection notes that an unfamiliar reviewer can use to reconstruct the loss conditions. This evidence base is what the carrier's expert needs to either accept or specifically rebut at deposition. When it exists and is complete, the carrier's expert generally cannot rebut it. When it doesn't exist, every line is exposed.

When all three layers are present from the moment the file is opened, the factor-fee argument has nothing to attach to. The work is technically defensible regardless of the financial structure around it. The carrier's defense team has to engage with the substance of the work, which they generally lose.

Three ways WCE works with funders without competing with your underwriting

WorldClass Estimates positions specifically as a technical estimating partner to funded portfolios. The position is structurally distinct from the funder's underwriting function. WCE does not assess advance-worthiness, does not score contractors for funding fit, and does not participate in the funder's commercial relationship with portfolio contractors. Three engagement structures cover the operational use cases:

Structure one — invoices written upstream of funding decisions. When a contractor in your portfolio needs an invoice written for a Florida loss, WCE writes it as the third-party estimator. The invoice carries WCE's technical standards by default — correct Xactimate sub-line selection, current Florida Building Code citations, ANSI/IICRC framework references for mitigation, Audit Report and Variation Report consistent with Rule 69BER24-4. The contractor takes the WCE-written invoice to the carrier. The funder sees a portfolio of invoices with consistent technical quality rather than wide variability.

Structure two — training delivered to the contractors in your portfolio. Workshops and webinars on Xactimate fundamentals, IICRC documentation, defending invoices against carrier pushback, and the factor-fee argument specifically. Branded as a value-add of your funding offering. The training raises the technical quality of every invoice in the portfolio over time.

Structure three — dispute recovery on stuck files. When a funded invoice has been reduced or has stalled in carrier review, WCE rebuilds the documentation to defensible standard and supports the resubmission or escalation. This is recovery work, not new origination work, and it directly affects collection on receivables already advanced.

None of these engagement structures involves WCE in the funder's underwriting decisions. The contractors remain the funder's commercial relationship. WCE provides the technical estimating function those contractors need to produce defensible invoices.

The 5-invoice portfolio audit

For funding companies considering whether the factor-fee argument is materially affecting recovery in their portfolio, WCE offers a no-cost audit of five invoices from your portfolio. The selection criteria: five recent invoices that were submitted to Florida carriers and either reduced significantly or stalled in carrier review.

The audit produces a written assessment of where each invoice was technically exposed, what the cuts attached to, and whether the technical fix would have prevented or mitigated the reduction. It does not assess the contractor's underwriting profile. It does not score the funded relationship. It looks only at the technical content of the invoice and the documentation around it.

The output is useful for two decisions. First, whether the factor-fee argument exposure in your portfolio justifies a structural intervention — training, third-party estimating, or both. Second, whether specific contractors in the portfolio are producing invoices that consistently fail in ways that affect recovery on advances.

Five invoices, one written report. No commitment beyond the audit itself.