Most Florida insurance carriers reduce more than half of every payout that crosses a desk adjuster's screen. The reduction is not random. It is not adversarial in the way clients sometimes assume. It is a systematic response to documentation that doesn't speak the carrier's language. The estimate gets cut because the cut is defensible — not because the damage wasn't real.

Public adjusters who have worked Florida claims for any length of time have seen this pattern. The challenge is what to do about it. The answer turns out to be narrower and more practical than most market commentary suggests.

The 60% number isn't about damage

The first thing worth saying clearly is that the 60% reduction figure isn't a reflection of bad faith on the carrier side or weak damage on the policyholder side. It reflects a documentation gap.

When a Florida desk adjuster opens a claim file, they are reading the estimate against three reference points: the carrier's internal cost data for the geography, the policy language and applicable endorsements, and any relevant industry standard for the type of loss. If the submitted estimate does not anticipate those three reference points and address them line by line, the reductions write themselves. The desk adjuster doesn't need to find a reason to cut. The reasons are already in the estimate, in the form of categorization choices, missing citations, and absent justifications.

The strongest PA estimates in Florida don't beat the carrier on price. They eliminate the room the carrier has to make a defensible cut. There is nothing left for the desk adjuster to argue with — not because the estimate is aggressive, but because every line is justified before the desk adjuster reaches it.

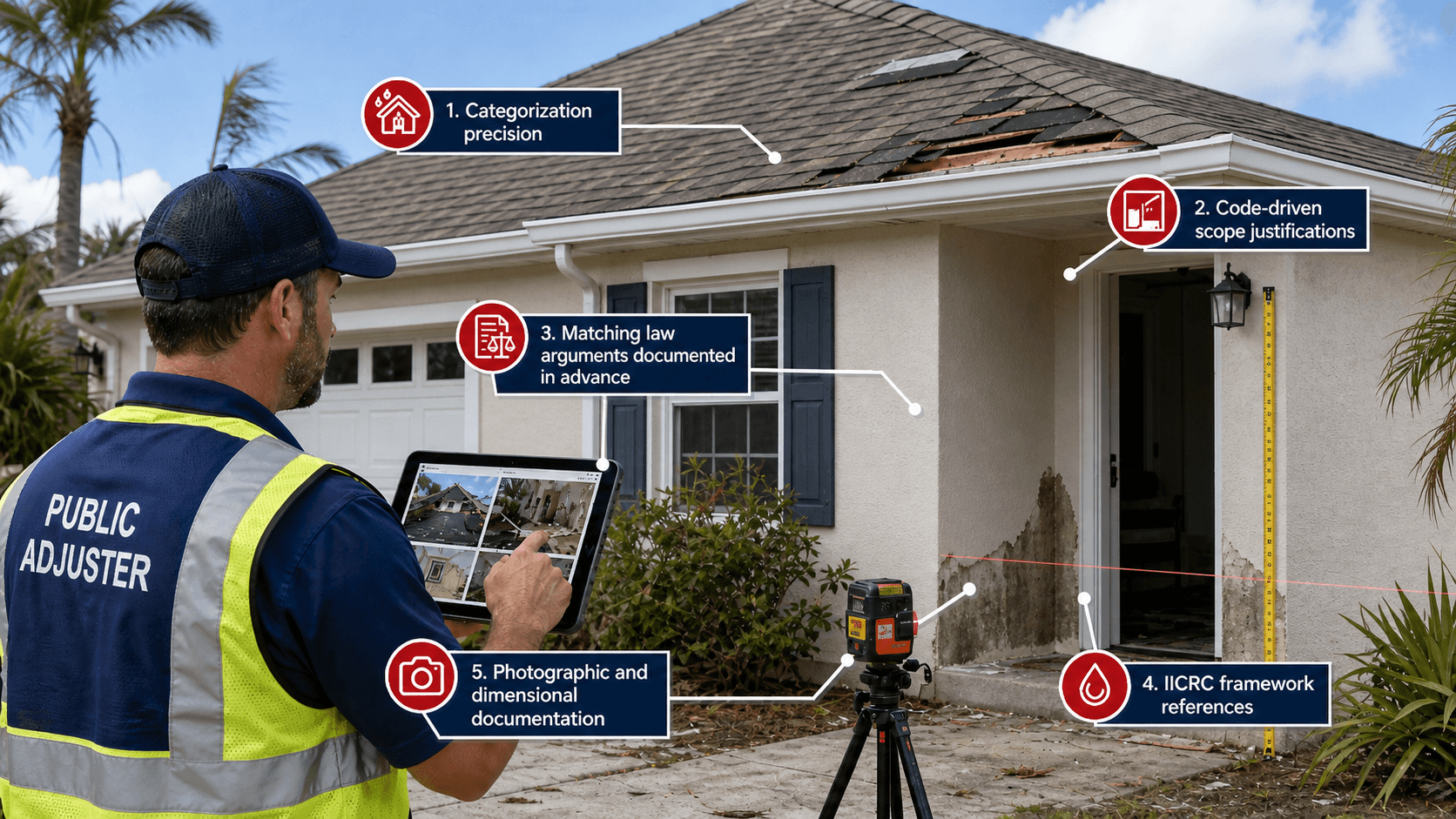

The five categories of writing the carrier looks for first

After 20,000-plus estimates across Florida claims, the patterns of what gets cut are consistent. Five categories of writing decide whether an estimate holds up:

Categorization precision. Xactimate has a sub-line architecture that most users never fully use. Generic line items like "drywall repair" sit at the top of an inverted tree of more specific options. The desk adjuster's automated review tools cross-reference your line item to expected scope. When you select a generic parent line, the carrier's review system substitutes their interpretation of what was actually needed — which is almost always cheaper. The fix is not aggressive selection. It is precise selection. Pick the most specific sub-line that matches the actual work, and the substitution argument goes away.

Code-driven scope justifications. Florida property claims live and die on code citation. Florida Building Code (8th Edition, 2023), the International Residential Code, the International Building Code, and local ordinances drive what materials must be used, what installation methods are required, and what triggers a code-upgrade payment. Estimates that cite the relevant section verbatim — with edition year — get treated differently than estimates that gesture at "code requirements" without specifics. The carrier's adjuster has to validate cited sections. They cannot validate vague references.

Matching law arguments documented in advance. Florida's matching principle requires uniform replacement of damaged building elements when partial repair would create visible discontinuity. Most PAs know the principle. Many learn it after the carrier has already cut the matching line items. The fix is to document matching arguments before the estimate is submitted: photographs showing visible discontinuity, dimensional evidence of pattern continuation, and citations to relevant Florida court decisions on matching. The matching argument made post-hoc is twice as hard as the matching argument made at intake.

IICRC framework references for water, fire, and mold work. When an estimate involves mitigation, the absence of references to ANSI/IICRC standards (S500-2021 for water, S520 for mold, S700 for fire) is read as absence of methodology. The carrier's reviewer doesn't need to claim the work was bad — they only need to claim the documentation doesn't establish that the work followed standard methodology. References to the standards by number and edition signal that the work was performed under recognized framework. Estimates without that signal get reductions on equipment days, antimicrobial application, PPE, and disposal — the four mitigation line categories that carry no documentary cost to cut.

Photographic and dimensional documentation that survives second review. Florida's Rule 69BER24-4 requires Audit Reports and Variation Reports for property insurance estimates. Beyond that statutory requirement, the operational requirement is photographic documentation that an unfamiliar reviewer — possibly a carrier's expert hired post-litigation — can use to reconstruct the loss without being on site. That standard of documentation is much higher than what most estimate photographs achieve. The fix is a photo grid protocol that captures every elevation, every transition, every code-relevant condition, and every line-item-relevant detail in a sequence that ties back to the scope sheet.

These five categories cover almost every reduction pattern that shows up in Florida desk-adjuster review. None of them are about being aggressive. All of them are about being defensible.

Xactimate categorization: the difference between a sub-line and a parent line

The single highest-leverage technical move in Florida estimating is correct sub-line selection in Xactimate. Most market discussion treats this as a software-skills issue. It is not. It is a carrier-review issue.

Consider drywall. The Xactimate library has dozens of drywall-related line items. A general "drywall repair" entry produces one outcome on review. "Detach & reset" produces a different outcome. "1/2-inch drywall - hung, taped, ready for paint" produces yet another. Each carries different expected price ranges, different scope assumptions, and different review tolerances on the carrier side.

When the wrong sub-line is selected, the desk adjuster's review tool generally accepts the line at face value but applies internal substitution logic — quietly mapping your selection to a cheaper alternative the system considers equivalent. The reduction shows up in the Statement of Loss without explanation. The PA who didn't write the estimate often cannot tell whether the cut was substantive or technical.

The same pattern appears across every category of work — flooring, roofing, framing, mechanicals, finishes. Selecting the most specific sub-line that genuinely matches the actual work eliminates the carrier's substitution path entirely. The line stands as written or the carrier has to argue against the substance of the work, not the categorization of it.

Code citations as defensive armor

Florida Building Code citations function differently from other technical citations because Florida law is public-domain regulatory material. A carrier's reviewer cannot dismiss a properly cited code section. They can argue about applicability, but they cannot argue about whether the section says what it says.

The discipline of citing code in a property estimate is straightforward. Identify the section that drives the scope choice. Cite it with edition year and section number ("FBC Residential, 8th Edition (2023) §R702.4"). Note the specific requirement the section establishes. Tie that requirement to the line item being claimed.

That sequence is short. It is also rarely done in PA-generated estimates. The estimates that include it are the estimates that come back from carrier review with the code-driven line items intact.

The 8th Edition (2023) of the Florida Building Code Residential is the current version as of the publication of this article. It is based on the 2021 IRC with Florida-specific amendments. Several section numbers shifted between the 7th Edition (2020) and the 8th Edition. Any code-citation library your firm maintains needs to be current to the 8th Edition.

What we do differently

WorldClass Estimates writes estimates in the format Florida carriers use to process automatic approvals. The work is structurally the same as what an experienced in-house PA estimator does — it is the application that differs.

Every line item is selected at the most specific sub-line. Every code reference is cited with edition and section. Every matching argument is documented before submission. Every mitigation line carries the appropriate ANSI/IICRC framework reference. The Audit Report and Variation Report mandated by Rule 69BER24-4 are produced by default for every Florida-loss estimate.

The Florida-specific compliance package is included in every estimate without separate request. Bilingual handling — every report, every call, every supporting document available in English or Spanish — is the default, not an option.

How a free case review works

If you have a case where the carrier is being difficult, send it for a no-cost review. The output is a technical assessment of where the estimate is exposed and what would change if it were rewritten. If the case is one we can help with, we'll talk about how. If it isn't, you keep the technical feedback either way.

The review is not a sales call. It is a second set of eyes on a technical document. That is sometimes all a difficult case needs.